.avif)

⋅ X min read

This is a Budget that reshapes elements of the tax system that underpin how organisations structure compensation. The introduction of a cap on NI-free pension salary sacrifice, the extension of fiscal drag, and new running-cost charges for electric vehicles amount to a material shift in the environment within which HR and payroll teams operate.

Some of the most widely trailed pre-Budget rumours — such as a cap on Cycle to Work — did not materialise. Others landed exactly as expected. For employers, the task now is to translate confirmed measures into operational changes, cost models and communication plans.

1. Salary Sacrifice for Pensions: The Most Significant Change for Employers

The most consequential measure for businesses is the introduction of a £2,000 annual cap on pension salary sacrifice contributions that remain exempt from National Insurance, effective April 2029.

For years, salary sacrifice has enabled both employees and employers to reduce NI costs through pension contributions. The new cap does not eliminate salary sacrifice, nor does it affect income tax relief, but it removes the NI efficiency above £2,000 — a meaningful change for organisations with generous matching schemes or high participation rates.

The business impact is extensive:

- Scheme redesign: Employers must review contribution structures and model new employer NI liabilities.

- Payroll systems: File formats, contribution flows and automated rules will require updates well ahead of 2029.

- Contractual and policy updates: Many employers will need to revise scheme documentation and communication materials.

- Budgeting: Employer NI costs will rise for organisations contributing above the threshold.

Importantly, this cap applies only to pensions. Other salary sacrifice schemes — EV, Cycle to Work and others — remain unchanged. This distinction will matter in employer comms to avoid conflation or confusion.

The change is likely to prompt some employers to rebalance their reward mix, placing greater emphasis on other benefits — particularly health and wellbeing support — as the relative NI advantage of higher pension contributions diminishes.

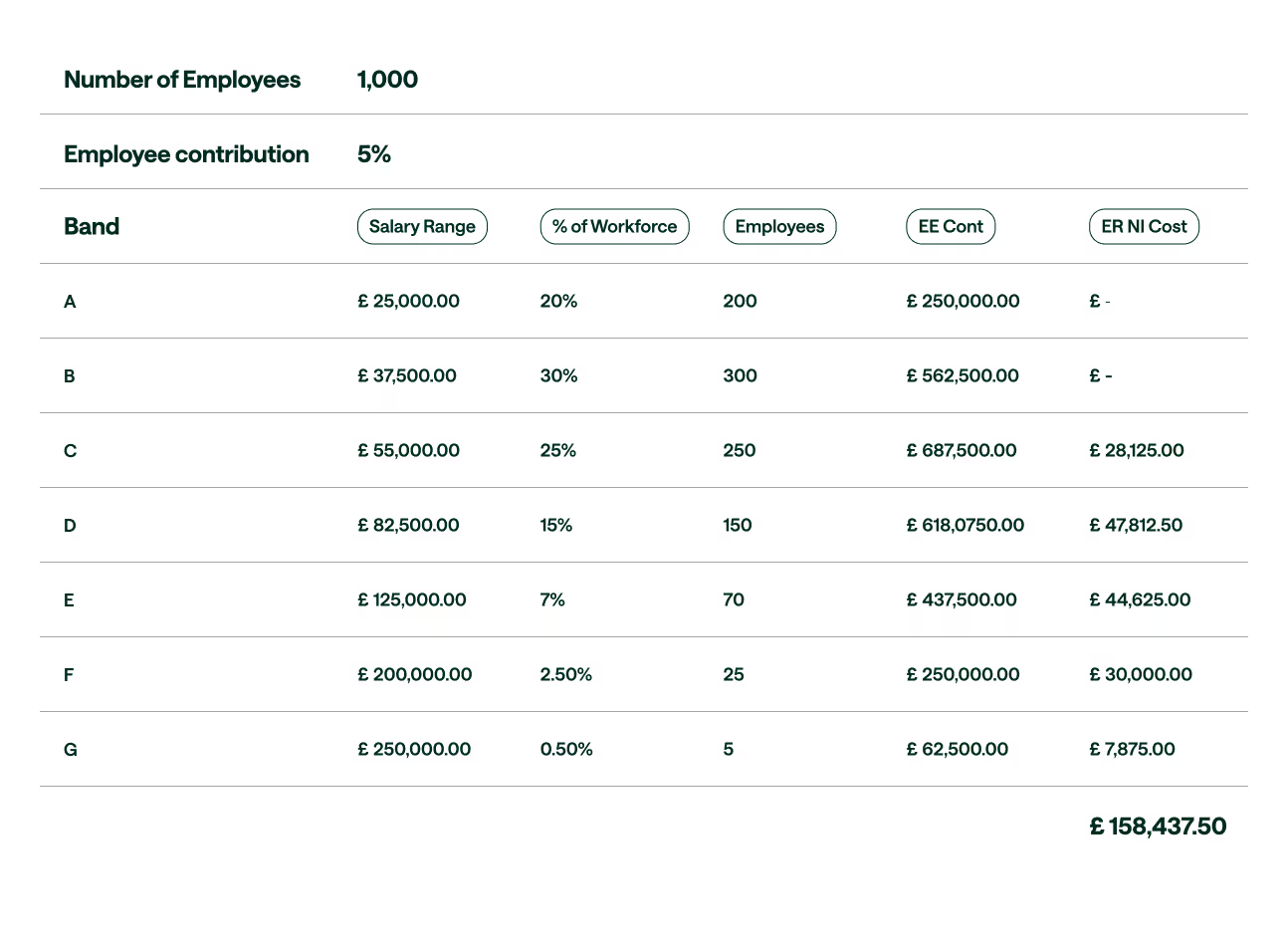

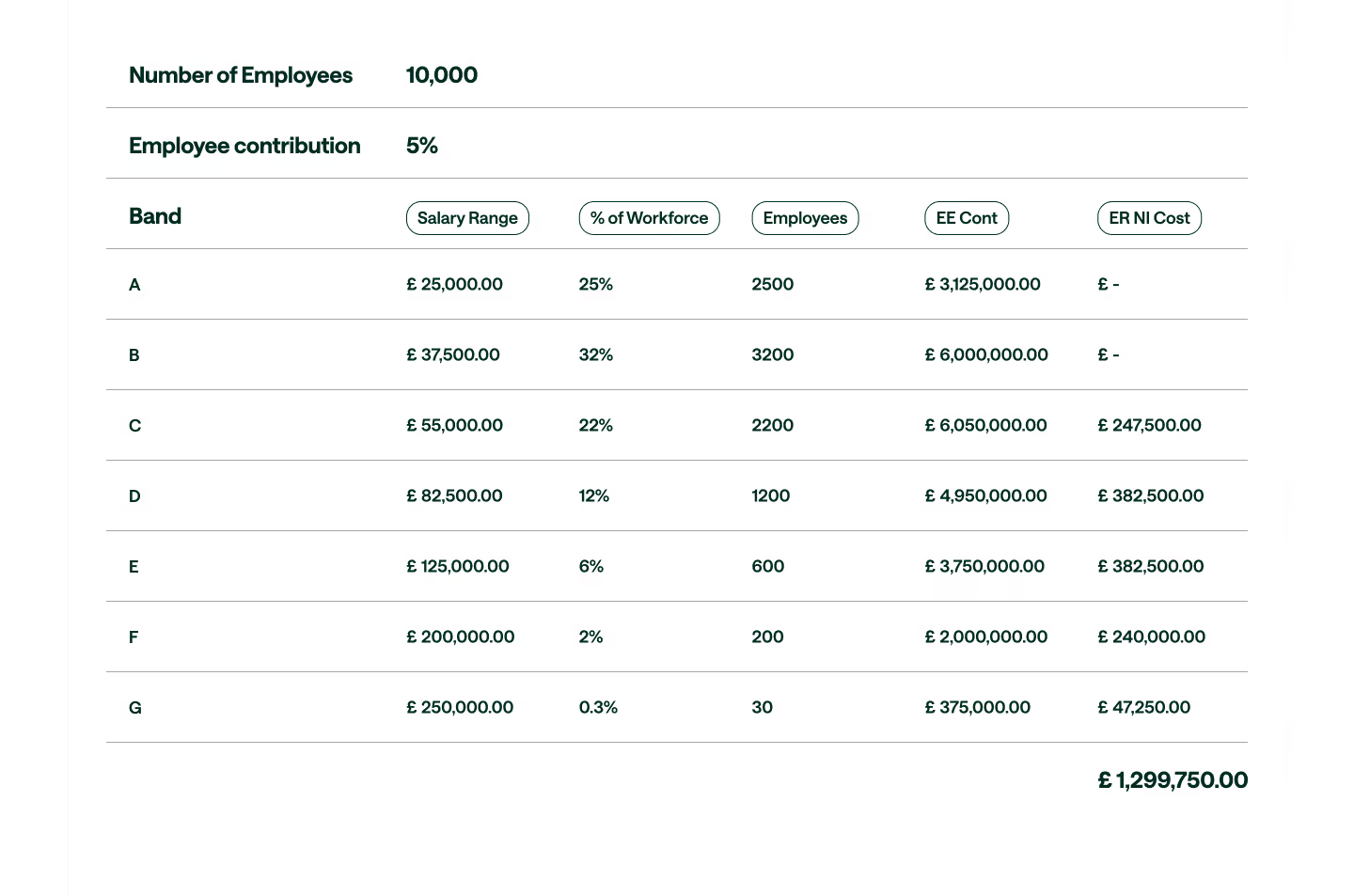

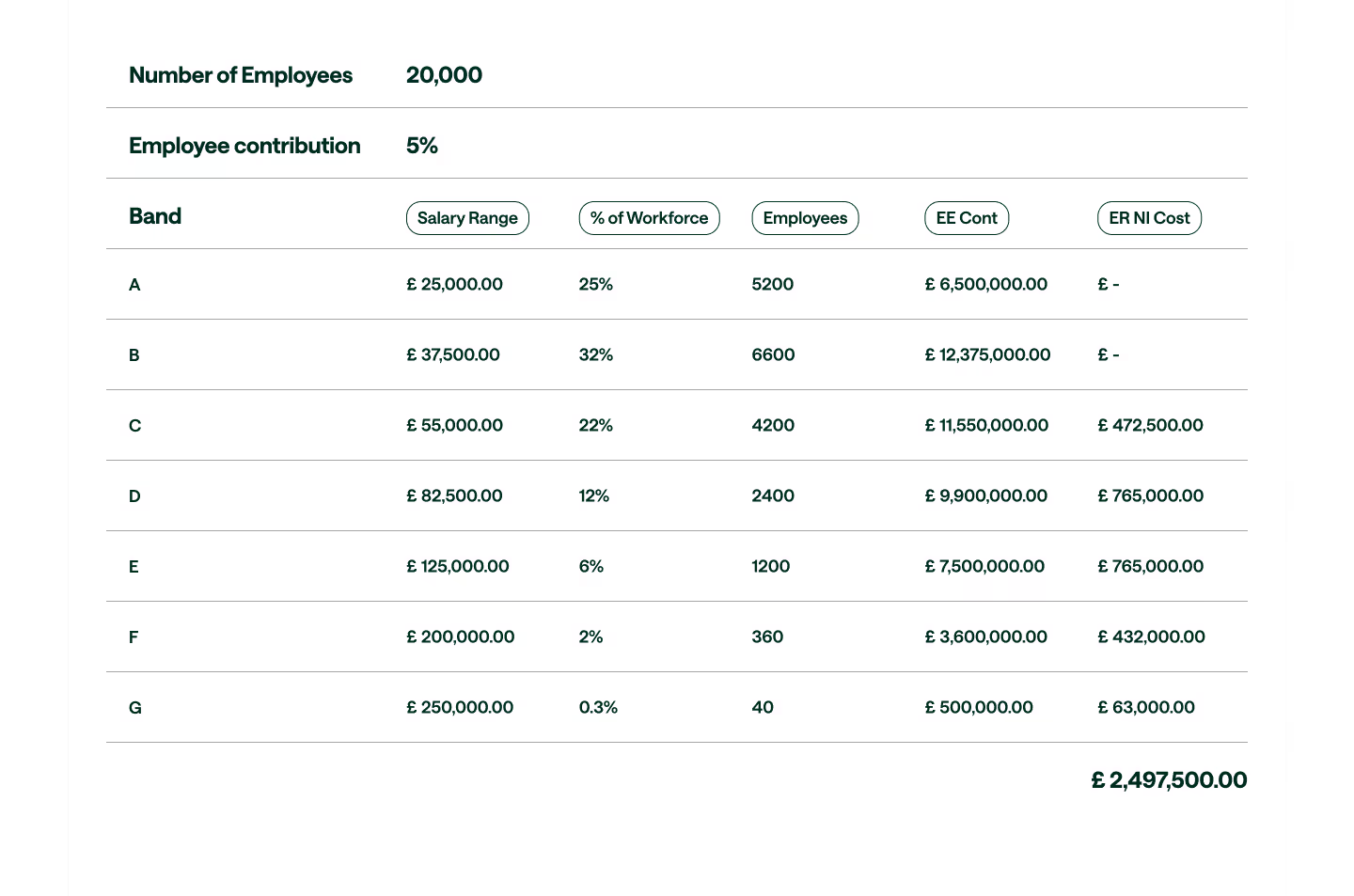

How much will this cost employers?

While the fiscal impact will vary by workforce profile, initial modelling shows the potential scale of employer NI costs once the cap takes effect.

These figures are illustrative and will differ based on employer contribution structures, workforce demographics and scheme participation levels, but they demonstrate the magnitude of the shift.

Carl Chapman, VP of Benefits at Ben, said the change will require employers to reassess their long-term approach to reward strategy:

“The cap on salary-sacrifice pension benefits may raise short-term revenue, but it risks weakening a vital, tax-efficient savings tool for employees. With changes not taking effect until 2029, the time is now for employers to act. This moment gives companies a real opportunity to reassess their wider benefits offering and take proactive steps to mitigate the additional cost, including ensuring that every pound of benefit spend is delivering meaningful return and real value for their people.”

2. Fiscal Drag Extended: Pay Awards Become Harder to Communicate

The Chancellor confirmed the extension of the income tax threshold freeze to 2031, ensuring fiscal drag will continue for at least another six years. While this does not impose new administrative duties on employers, the effects will be felt directly in annual pay cycles.

As wages rise — even modestly — more employees will cross or move deeper into higher tax bands. This reduces the net value of pay awards and complicates employers’ attempts to maintain competitiveness during pay rounds.

For HR leaders, the implications are:

- Higher employee challenge: Workers may perceive net pay erosion even as organisations increase salaries.

- Pressure on remuneration budgets: Employers may face calls for larger nominal pay rises to offset higher tax exposure.

- A greater role for non-salary benefits: Organisations will need to articulate value beyond simple pay increases.

3. Electric Vehicles: New Running-Cost Charges from 2028

The Budget confirmed a 3p-per-mile tax on electric vehicle usage from 2028. EV salary sacrifice schemes have been one of the fastest-growing benefits in the UK, driven by low benefit-in-kind rates and predictable running costs.

The new charge does not alter the structure of salary sacrifice schemes themselves, but it changes the economic assumptions organisations use when communicating their value.

Employers should now expect:

- Demand for updated total cost of ownership modelling, including the new variable running cost.

- Potential adjustments by lease providers, especially where mileage reconciliation occurs at end of contract.

The change is not destructive to the benefit, but it introduces new complexity.

4. Cycle to Work: No Cap Introduced, Contrary to Expectation

One of the most significant surprises of the Budget for employers was what did not happen.

Despite extensive speculation, the government did not introduce a £1,000 cap on Cycle to Work purchases. The scheme continues unchanged — an outcome welcomed by industry figures.

As Jamie Milroy, CEO and Founder at DASH, said:

"This is welcome news for the Cycle to Work scheme and the wider UK cycling industry. The rumoured cap would have unfairly discriminated against those whose needs necessitate higher-value bikes and e-bikes, such as parents using cargo bikes for the school run or individuals requiring specially adapted cycles.

With cycling levels up 43% versus 2019, the continuation of the Cycle to Work scheme ensures this momentum is not lost, along with the significant financial and well-being benefits cycling provides to employees."

The absence of a cap means employers do not need to modify existing schemes or alter procurement frameworks for e-bikes and cargo bikes. For organisations promoting sustainable travel or supporting longer-distance cycling commutes, this provides welcome continuity.

5. ISA Changes: Limited Immediate Employer Impact, but Likely Increased Demand for Guidance

The Budget also confirmed changes requiring that part of the £20,000 annual ISA allowance must now be allocated to stocks and shares investments.

There is no direct administrative requirement for employers, but experience suggests employees could turn to their workplace for guidance.

This typically increases demand for:

- financial wellbeing tools

- savings explainers

- reward platform content

- integrated financial modelling

While the change is not operationally burdensome, it could increase the informational burden on HR teams.

6. A More Complex Landscape for Organisations

Across all the confirmed measures, the central theme for employers is increasing complexity.

Unlike previous Budgets that sought to simplify or consolidate elements of tax policy, this one introduces new thresholds, new caps, new calculations and new running-cost variables.

For HR, reward and payroll teams, that means:

- revisiting contribution structures

- recalculating employer costs

- reprogramming payroll systems

- updating scheme documentation

- communicating changes clearly and quickly

- preparing for higher volumes of employee queries

The pension changes also raise a broader strategic issue for employers. With the NI advantage on higher pension contributions reduced, organisations are likely to place greater weight on other forms of reward — particularly health and wellbeing benefits.

Together, these shifts ensure that reward strategy will need to be broader, more adaptive and more closely linked to workforce health and resilience.

Conclusion: A Widely Scrutinised Budget With Targeted but Significant Consequences for Employers

The 2025 Budget has already attracted extensive political and public attention, and its business implications are equally substantial.

The targeted cap on NI-free pension salary sacrifice is the most structurally significant change, but the extension of fiscal drag and new EV running-cost charges also reshape the strategic environment for reward.

None of these measures require employers to abandon existing benefits. But they do require organisations to adjust systems, review schemes, update documentation and provide clearer information to their workforces.

This is likely to bring greater emphasis on workplace health support, wellbeing provision and broader reward diversification as employers look for value beyond pension tax efficiency.

This is a Budget that delivered fewer surprises than expected, but its measures will shape payroll operations, pension policy and reward strategy for years to come.

For HR, reward and benefits leaders, the work of interpreting and implementing these changes begins immediately.

.avif)

.jpg)